|

|||

|

|

House of Representatives Standing Committee on Communications

Navigation: Previous Page | Contents | Next Page Chapter 3 Previous reports on international mobile roaming3.1 In the previous chapter, the Committee described how the administrative and technical framework of roaming contributes to the cost of this service. Even with the technical nature of roaming, charges are considered high, with both the Consumers’ Telecommunications Network (CTN) and the Australian Competition and Consumer Commission (ACCC) making this point.[1] 3.2 Two reports on Australian international mobile roaming charges have been published in recent years:

These reports provide an insight into the underlying price components of international mobile roaming services. 3.3 Both reports investigated a range of issues including:

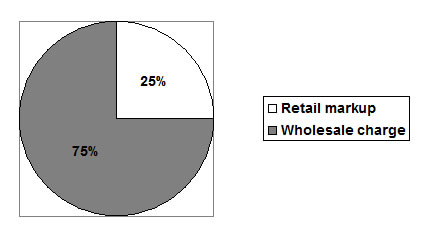

Report findings3.4 Both reports contain a number of similar findings about how the person who subscribed to the roaming service (described as an ‘end user’) is charged. Wholesale charge3.5 The wholesale part of the end user price reflects the Inter Operator Tariff (IOT) charge as negotiated between the home network operator and the visited network operator.[3] 3.6 Optus provided the Committee with some insight as to how these wholesale arrangements are agreed upon and passed on to consumers. Optus asserted that carriers negotiate the best wholesale price they can with the visited network operator, then reflect this wholesale price in their end prices to consumers.[4] 3.7 The Committee also heard evidence as to how these wholesale transactions occur. When a call is made on a visited network, the billing personnel of the visited network compile a billing file with the details of the call and the wholesale charges associated with it. This billing file is then sent to a clearing house where the file is distributed to the home network operator. The home network operator then pays the wholesale charges as recorded in the billing file.[5] 3.8 These wholesale costs are incurred by the home network operator whenever one of their subscribers makes a call on a visited network. The home network operator then attempts to recover these wholesale costs by including them in the retail roaming bill to the subscriber who made the call. 3.9 The Australian Mobile Telecommunications Association’s (AMTA’s) submission to the inquiry highlighted that, due to this wholesale arrangement, home network providers shoulder some amount of risk to facilitate the roaming service. The submission stated: … IOT charges are paid to the visited network by the home network irrespective of whether the home network recovers any fees from its customer. The home network operator therefore takes on all bad debt risk (i.e. the risk of the non-recovery of charges from the end customer).[6] 3.10 The Committee heard evidence that this wholesale billing method can cause delays to the billing of international mobile roaming charges to the end user. The CTN stated that sometimes providers are unable to provide current balances of international roaming charges to their customers because of delays in receiving billing information from visited network providers.[7] However, Vodafone Australia argued that these delays are an exception to the rule.[8] Home network operator’s mark-up3.11 The ACCC determined that the mark-up component of roaming retail charges is not governed by any common set of principles. Rather, each home network operator is free to determine the size of the mark-up component of the retail price. The ACCC suggested that usually this mark-up is determined by adding a percentage of the IOT onto the wholesale charge as negotiated in the party-to-party agreement.[9] 3.12 Telstra advised that the mark-up varies depending on both the carrier and the destination country in which the subscriber uses international roaming.[10] 3.13 A range of evidence was provided to the Committee as to how the size of these retail mark-ups are determined by carriers. Operational costs3.14 First, many home network providers asserted that there are significant operational costs that must be recovered by providers through the retail mark-up. For example, Telstra pointed out that retail mark-ups must cover the operational costs of the home network operator including front-of-house customer service, customer support and customer billing costs.[11] 3.15 AMTA argued that the mark-up component of the retail price covers the costs of negotiating and administrating party-to-party roaming agreements, marketing, customer support as well as cost associated with the maintenance and construction of the network operator’s infrastructure.[12] 3.16 Vodafone Australia added the operational costs associated with facilitating wholesale transactions is included in the retail mark-up to the list. According to Vodafone Australia, the operation of the clearing houses, where the wholesale billing information is transacted can be quite costly. The cost of operating of these clearing houses must be recouped by the home network provider by including the cost in the retail mark-up.[13] Bundling3.17 Another factor contributing to the home network providers’ mark-up was the bundling of roaming with other mobile phone services. 3.18 Vodafone Australia stated that its international mobile roaming service comes bundled with a range of other mobile services, such as domestic voice and SMS. Thus, revenues to Vodafone from the retail mark-up on roaming may allow it to reduce the mark-up applied to other high-demand mobile services within the bundle. This makes the bundle more attractive to a wider range of consumers.[14] Premium service3.19 Finally, there was a consistent view amongst the providers that international roaming was a premium service and that this may be a factor considered by providers when determining the size of the mark-up on the service.[15] In other words, international mobile roaming is considered to be a privilege type of service, attracting a commensurate cost. ACCC report3.20 The size of the IOT tariff is negotiated between providers and can be expected to vary depending on the home network operator’s call volume, customer expenditure, call volume growth and destination of calls as well as the number of providers in the foreign country.[16] 3.21 In order to investigate what proportion of the final consumer price of roaming is attributable to the wholesale price and what proportion is attributable to the retail mark-up charged by home network providers, the ACCC used publicly available information from Telstra stating that the retail mark-up for their outbound international roaming services is 30 percent. Using the Telstra figures, the ACCC extrapolated a general figure for the Australian market of a 25 percent markup.[17] 3.22 Given this 25 percent retail mark-up, the report infers that wholesale charges make up 75 percent of the final price charged to consumers.[18] This conclusion is illustrated below. Figure 3.1 – ACCC’s conclusion regarding wholesale and mark-up components of final consumer price

3.23 According to the ACCC, the size of the wholesale charge is based on the profitability of an Australian operator’s customer base and the nature of the visited network providers.[19] 3.24 The BDCDE suggested that network providers who have a relatively small share of the global international roaming market, such as many Australian providers, are inevitably price takers when it comes to party-to-party agreements:[20] …[Australian network operators] tend to be price takers rather than price setters. They are often confronted with negotiating roaming agreements with, in some cases, a limited number of alternatives and they are often negotiating with existing alliances of international carriers, so they are confronted with existing pricing arrangements. [21] 3.25 According to the ACCC, another factor affecting IOT pricing is the number of providers in a country. Where there are the least number of mobile providers in a country, IOTs are likely to be highest.[22] 3.26 Industry representatives generally agreed with this assessment. Vodafone Australia supported the arguments put forward by the DBCDE and the ACCC, advising the Committee that the scope, scale and volume of the Australian international roaming market puts most Australian providers at a disadvantage when negotiating IOTs with foreign providers.[23] 3.27 However the Committee also heard evidence that some network providers are in a position to limit the impact Australia’s small volume has on their negotiating power. Vodafone Australia, a subsidiary of the Vodafone Group which has a presence in twenty six countries,[24] is sometimes able to take advantage of this global presence when negotiating prices.[25] 3.28 Another possibility for limiting the impact of Australia’s small volume is for Australian providers to become members of inter-carrier alliances. The ACCC’s submission to the inquiry notes the emergence of inter-carrier alliances that allow network providers from different countries to form a coalition to negotiate IOTs with other larger network providers, increasing the negotiating power of the providers.[26] The DBCDE was also of the view that some Australian providers are no longer price takers due to participation in such alliances.[27] 3.29 There are two weaknesses in the ACCC’s analysis. The first is its extrapolation from publicly available Telstra figures on the retail mark-up to all Australian providers. This weakness is quite difficult to overcome because of the commercial in confidence nature of this information. In other words, the ACCC could not obtain the same information from other providers. 3.30 The second weakness is the age of the report. The report was published in 2005 and was based on information obtained some years earlier. In the mobile phone market, that is enough time for substantial changes to have occurred. KPMG report3.31 KPMG’s investigation employed a different method to the ACCC’s analyses. KPMG used publicly available international benchmark data, published by the Technical University of Denmark, to estimate the actual per-minute costs of providing an international mobile roaming service and the average retail cost per-minute to consumers of this service. These costs were then converted to Australian dollars. These estimates include the actual costs associated with termination rates, international call transit rates and roaming specific costs.[28] 3.32 To determine the approximate mark up applied to a roamed call by the overseas and Australian providers, the report deducted the total estimated actual cost from the average end user cost.[29] The figures for this analysis are illustrated in the table below. Figure 3.2 – KPMG’s analysis of wholesale and mark-up price components

Source: Department of Broadband, Communications and the Digital Economy, Report of findings on international mobile roaming charges, 2008, p. 23.3.33 Figure two shows that KPMG determined that where a consumer pays $2.75 per minute for an international mobile roaming call, $0.46 of this per minute charge is accounted for by the actual cost and $2.29 by the mark up applied by the overseas and home network providers. 3.34 Figure three demonstrates KPMG’s conclusion as a percentage. Figure 3.3 – KPMG’s conclusion regarding actual cost and mark-up components of final consumer price

Source: Department of Broadband, Communications and the Digital Economy, Report of findings on international mobile roaming charges, 2008, p. 23.3.35 The disadvantage of this approach is that the actual cost of the roamed call is not what Australian providers are charged. As has already been discussed, the Australian market has some specific peculiarities, such as being a small market with little bargaining power in international negotiations over IOT tariffs. This could mean that the Australian situation is very different. Different approaches by the ACCC and KPMG3.36 Whilst both the ACCC and KPMG analyses are validly based, the Committee notes that the ACCC and KPMG reports each adopt a different approach to investigating roaming, leading to findings that emphasise different aspects of the roaming market. The ACCC’s approach focuses attention on the role played by the party-to-party agreements in determining the end user cost. KPMG’s approach directs attention to the discrepancy between the actual cost of roamed calls and the end user cost. 3.37 In doing this, the KPMG report relies on international benchmark cost information and then assumes that Australian providers are charged this actual cost for roamed calls by overseas providers. The ACCC, on the other hand, has relied on publicly available information directly from a single Australian carrier and extrapolated this to all Australian service providers. 3.38 It should also be noted that the ACCC has investigative powers which provide it with information resources, and an understanding of Australian markets, largely unavailable to private-sector consultancy firms. 3.39 The Committee asked the ACCC to comment on KPMG’s findings. The ACCC suggested that: ...the KPMG 2008 Report appears to correctly identify the actual component costs of providing a roamed call … as being quite small compared to the charges faced by the end-user. However, no account appears to have been made of the wholesale charges levied by [visited network operators].[30] 3.40 The ACCC also suggested that the benchmark cost information provided by the Technical University of Denmark, and used in the KPMG report, may underestimate the component costs of transmitting a mobile call to and from Australia. The transmission of mobile calls between northern hemisphere countries, which make up the bulk of international call traffic, cover much smaller distances, and may use significantly less resources, than transmitting a call between Australia and Europe.[31] 3.41 When carriers were asked to comment on the reports, they suggested that the ACCC’s analysis was a better reflection of the reality of roaming arrangements. Telstra, for example, suggested that the conclusion of the ACCC was accurate when compared to their cost data.[32] 3.42 Vodafone Australia concurred, stating that the wholesale price paid by home network providers to visited network providers constitutes the biggest component of the end user price to consumers.[33] 3.43 The Committee is of the view that, while both the KPMG and ACCC reports are based on valid sources, neither entirely reflects the pricing situation as both rely on extrapolating conclusions rather than direct data, and that as a consequence, both are flawed. Market distortions3.44 In the case of roaming services offered by Australian providers, the Committee considers that the market does not operate effectively because the size of the Australian population reduces competition. Australian providers cannot offer enough customers to providers in other countries to make negotiations over price competitive. 3.45 In addition, Australian customers do not generally choose their provider on the cost of international mobile roaming, but on the domestic charges. 3.46 The result of this distortion is that the price of roaming in Australia is high, and the product is considered by Australian providers to be a premium service. 3.47 In the next chapter, the Committee considers what can be done to ameliorate this distortion. |