|

|

|||

|

|

|||

|

|

|

|

|

|||||||||||||||||

Recommendation 11 |

|

|

5.44 |

Where the ATO has concerns about a judicial decision, it should publicly announce these concerns in the decision impact statement and commit to resolving the issue within 12 months through one or a combination of the following public actions: n abiding by the initial decision n appealing the decision and abiding by any subsequent decision n referring the issue to Treasury as a policy matter. |

5.45 Similar to judicial changes in interpretation, the ATO may itself decide that its interpretation of the law is incorrect or may update its advice on how to comply with the law. An example of the former is agribusiness investment schemes. At the biannual meeting with the Commissioner on 20 April 2007, the ATO advised the Committee how it came to develop its new position on the law:

What we have actually had is indications from the court—one by the Supreme Court in Environ and another one by the Federal Court in Puzey—to say that our view of the law was wrong…

…it has taken some time. We then referred the matter to government because it was really a government issue of how it wanted these areas taxed. The government made its decision in relation to afforestation and decided that we should just test the law—it said it would not do anything in relation to agriculture or agribusiness. That left the tax office with views expressed by the judiciary that our previous view was not right. We have gone through an extensive process of trying to review our position. We think a better view now is that we were wrong. Therefore, we are trying now to have a test case to clarify that over the next 12 months.

Last week we issued a draft ruling reflecting that change of view.[44]

5.46 On 6 February 2007, the then Government announced that it would not extend the agribusiness tax concession to non-forestry schemes. The ATO’s initial position was that the new legal position would apply from 1 July that year.[45] This led to significant movements in the share prices of some agribusiness firms.[46] After significant community concern, the ATO announced on 27 March 2007 that it would not apply its new view of the law until 1 July 2008.[47] In effect, it granted a 12 month transition period.

5.47 An example of the ATO updating its advice to taxpayers in relation to compliance is service entities. In the 1978 case of Commissioner of Taxation v Phillips,[48] the Full Federal Court dealt with a situation where a business set up a separate entity to provide administrative services to it. The service entity was owned by the business owner’s family and, by directing profits from the business to the entity, was a form of income splitting. The Court permitted the arrangement because the entity provided the services at commercial rates.[49]

5.48 In that case, the service entity used a mark up of 50% on the direct costs of the employees providing the administrative services. The ATO released a short ruling (IT 276) after Phillips where it accepted the result, but did not make reference to specific mark ups. The Inspector-General of Taxation has reported that the ATO’s internal assessing manuals, publicly released in 1985, accepted the 50% benchmark on staff costs.[50]

5.49 In 2002, the ATO formally decided to address compliance issues related to service entities. It released draft guidance in 2005 and finalised it in 2006. In addition to other measures, the guidance limited the mark up on direct staff costs to 30%. The ATO announced that taxpayers had a 12-month period of grace in which to change their existing arrangements to meet the new standards.

5.50 In his report, the Inspector-General concluded that the ATO had changed its administrative practice. The ATO disagreed with this conclusion. The Committee does not wish to consider such matters of interpretation. What is important to note is the ATO gave taxpayers 12 months in which to comply with the new standards. The Committee believes that such periods of grace, when used appropriately, are fair on taxpayers.

5.51 The Committee accepts that the ATO may change its opinion of the law or may establish new benchmarks for complying with the law to accommodate changes in business practices. The Committee also believes that, once it has come to such a conclusion, the ATO needs to act promptly to satisfy taxpayers that it is enforcing the law. Firstly, this involves making a public announcement of its change of view. Secondly, the ATO may need to give taxpayers a period of time in which to change their affairs. Unless there are exceptional circumstances, such a period should be no longer than 12 months. This will be long enough for any adjustment, but any longer period would lead to doubts that the ATO is committed to enforcing the law. The length of the adjustment period will depend on the circumstances in each case and may need to be varied to take into account timing issues such as the end of the financial year.

5.52 Such a decision involves considerable discretion. The Committee is of the view that the ATO should develop a policy to ensure that these decisions are robust.

Recommendation 12 |

|

|

5.53 |

The ATO develop a policy to support decisions involving periods of grace where it changes its view of the law. Unless there are exceptional circumstances, no period of grace should exceed 12 months. |

5.54 The management of non-compliance, such as through investigations and audits, is a sensitive area in tax administration. The Ombudsman advised the Committee that a large number of complaints involve compliance activities:

The ATO’s compliance activities are an area about which the Ombudsman’s office receives a substantial number of complaints — generally over five hundred complaints each year (or about a third of all tax complaints). Most complaints relate to assessment, audit and recovery action.[51]

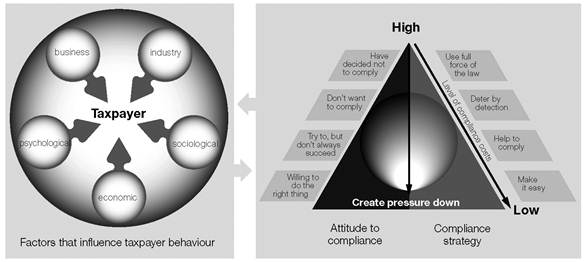

5.55 In examining the ATO’s compliance activities, the Committee found that the most suitable benchmark is fairness. In some respects, this is not surprising. The ATO investigates and audits taxpayers, amends their assessments and takes some taxpayers to court. This is similar to police action and prosecution. Therefore, it is natural to apply principles of legal fairness to the ATO’s compliance activities.

5.56 Earlier in the chapter, the Committee noted evidence that the main benefit of compliance work is it ensures that the proportion of compliant taxpayers remains high. Its secondary purpose is to raise revenue. The ATO advised the Committee that the return on compliance overall is $15 in revenue raised for every dollar spent on compliance work.[52]

5.57 The ATO stated that it takes a risk-based approach to audit and investigation:

… the way we select for audit activity is on the highest risk. The whole approach is to try and focus on outliers as a way of protecting the voluntary compliance of those who are doing the right thing.[53]

5.58 A large component of this work involves data collection and analysis. The ATO’s submission stated:

We verify compliance by reviewing high-risk cases and businesses with more complex arrangements. Our interactions with businesses range from checking claims by telephone and written requests through to intensive audits. Identifying high-risk cases involves matching large volumes of data to identify omitted transactions and businesses operating outside industry or economic norms.

We use the same techniques to identify businesses that represent little or no risk to the revenue system so that we avoid intruding on their affairs unnecessarily.[54]

5.59 The Committee supports the ATO reducing its compliance focus on law abiding taxpayers. The Commissioner gave an example of a conversation he had with a newsagent that shows there are costs involved in exposing compliant taxpayers to investigations:

I was in charge of the area that was looking at it at the time. He said to me: ‘Your people audited me. They did a good job, they were very professional and I did not have a problem, but I am really dark on the tax office and I will remain dark forever on them.’ When I asked why, he said, ‘Because you audited me and I have been trying to do the right thing, but you did not audit the person across the street, who is a crook.’ So there is a perception there that, if you just do randoms and you pick the wrong people, it actually reduces community confidence rather than increases it.[55]

5.60 The Committee supports the ATO’s risk-based approach to compliance. It directs the ATO’s resources to the areas of greatest need and does not burden compliant taxpayers.

5.61 In chapter one, the Committee discussed the various reasons why taxpayers in the mass marketed investment schemes felt the ATO had unfairly treated them. One of the main reasons was the ATO’s delayed reaction to the schemes. If taxpayers were not picked up by the ATO within 12 months of them lodging a return, it tended to create a precedent for the future. In its report on the schemes, the Senate Committee stated:

Although the ATO advised that it acted within 12 to 18 months to deny deductions claimed in up to 90 per cent of cases, in some instances the time lag was approximately two to three years, and in others the delay reached up to six years.[56]

5.62 Around this time, the ATO had significant powers to amend a taxpayer’s assessment. The standard period was four years. For taxpayers with a shorter period of review, the time was two years. These taxpayers needed to be individuals with simpler affairs, such as only deriving withholding income, using a limited range of deductions and incurring no capital gain or loss. In 2004, the ATO estimated there were 1.5 million taxpayers in this group. The standard period extended to six years where the ATO invoked Part IVA of the Income Tax Assessment Act 1936 (the general anti-avoidance provision).[57]

5.63 As part of RoSA in 2004, Treasury recommended that these time limits be reduced. In particular, businesses that elect to participate in the Simplified Tax System and individuals should have an amendment period of two years. Treasury recommended that partners of partnerships and beneficiaries of trusts that have not elected to participate in the Simplified Tax System should be excluded. Taxpayers subject to Part IVA (the general anti-avoidance provisions) had their amendment period reduced from six years to the standard four years.

5.64 The Parliament amended the tax laws in the Tax Laws Amendment (Improvements to Self Assessment) Act (No. 2) 2005 to give effect to these proposals. Under section 170 of the Income Tax Assessment Act 1936, the ATO has an unlimited period in which to amend an assessment if the Commissioner is of the opinion there has been fraud or evasion. This power is unchanged.

5.65 One of Treasury’s recommendations in RoSA was that it should further investigate the specific legislative instances where the ATO has an unlimited period to amend an assessment. There are over 100 of these. Treasury has released a discussion paper on this, proposing to group the provisions into four categories:

n converting to the standard two and four year assessment periods

n having a longer, finite period such as eight years

n where the provision relies on a contingent event, changing to two years after the event

n remaining an unlimited period.[58]

5.66 In RoSA, Treasury noted most individual taxpayers have very simple affairs. For them, the main compliance activity that the ATO conducts is processes such as income matching.[59] It is straightforward for the ATO to complete this within two years, especially now that data matching has reached a sophisticated and comprehensive stage.[60] Hence, the RoSA recommendations sensibly balance the requirements of ATO systems and the needs of taxpayers.

5.67 The Committee also supports the principles behind the recent Treasury Discussion Paper, which states:

Improving taxpayer certainty is a key goal for tax administration. The length of time that elapses before assessments can no longer be amended represents an aspect of risk and uncertainty for taxpayers. Unlimited amendment periods represent an extreme case of uncertainty, as the time to amend extends indefinitely. If that time can be limited without prejudicing the integrity and function of the system overall, the ‘costs’ of risk and uncertainty would be reduced.[61]

5.68 Tax stakeholders supported the announcement of this review.[62] It is still ongoing, so the Committee sees no need to make a recommendation.

5.69 The date at which an audit starts is important because it affects the value to a taxpayer of making a voluntary disclosure to the ATO.

5.70 Where a taxpayer incurs a tax shortfall amount, their conduct may warrant the imposition of an administrative penalty. The ATO decreases the base penalty if the taxpayer tells the ATO about the shortfall. The reduction depends on when the taxpayer makes the disclosure. If the taxpayer does so before an audit commences, then the reduction is 100% for a shortfall of less than $1,000 or 80% for a shortfall of $1,000 or more. If the taxpayer tells the ATO after an audit starts, the reduction is 20% if the disclosure saves the ATO significant time or resources.[63]

5.71 In 2005, the Inspector-General of Taxation released two reports that referred to taxpayer confusion over whether certain ATO compliance activities were audits and their commencement date. For instance, the report into audit timeframes stated:

A review of sample cases revealed that an audit commencement letter or phone call had not been sent or made in 11 out of 203 (5.42 per cent) audit case files reviewed where it was appropriate to notify taxpayers of the commencement of audits and where the case file was adequately maintained.[64]

5.72 The audit timeframe report noted that the ATO was resolving this issue in consultation with tax professionals through the Accountants Tax Practitioners’ Forum Audit Working Group. It recommended that the ATO ensure it complied with its procedures on notification of audits.[65] The penalties and interest report recommended that the ATO provide clearer guidance on when an audit starts and give taxpayers an opportunity to make voluntary disclosures prior to an audit formally commencing.[66]

5.73 In submissions, the ICAA[67] and the Taxation Institute of Australia expressed concern about how to ascertain when some audits start. The latter stated there was:

… considerable confusion at present about whether an ATO compliance activity constitutes an audit or not, with ramifications for whether a taxpayer can make a voluntary disclosure and seek to minimise the impact of any penalties. The ATO needs to put in place protocols for advising taxpayers about whether or not a particular compliance activity is an audit, and if so, when the audit commences. Although work has progressed in the ATO, resolution has stalled …[68]

5.74 The Committee appreciates that not all taxpayers should be told when an audit into their affairs commences. However, the Committee believes that taxpayers should be advised as often as possible, including borderline cases. This is consistent with legal principles of fairness. The Committee also notes that the ATO has commenced rectifying this problem but has not finalised the task. This should be completed as soon as possible.

Recommendation 13 |

|

|

5.75 |

The ATO establish and monitor compliance of protocols for determining when an investigation is an audit, when the audit commences, and when the ATO should inform the taxpayer of the audit. |

5.76 A feature of the ATO’s response to employee benefit arrangements was that it issued assessments for the transactions which were conditional on each other. In its press release for Essenbourne, the ATO stated that it did not pursue the fringe benefits tax assessment because it rendered the scheme ineffective by disallowing the income tax deduction.[69] In Pridecraft in the first instance, the ATO’s submission stated it would not follow up the fringe benefits tax assessment if it was successful in relation to the income tax deduction.[70]

5.77 The use of conditional (or multiple) assessments provoked a strong response from some taxpayers during the inquiry.[71] For instance:

The issuing of multiple assessments had participants amassing levels due to the ATO up to ten times the level of the actual participating sums. What a disgrace that any creditor let alone the ATO can take such a scatter gun approach. Every company and every participant has their ‘breaking point’ and the ATO did their best to find it.[72]

5.78 In evidence, the ATO stated that its goal was to ultimately pursue one assessment:

… our ongoing position is that we will settle on one point. If a case is in the court and the person has decided not to settle, we still put before the court the full range of options. But our position has been all along that we only collect on one taxing point and we only settle on one taxing point.[73]

5.79 The ATO also advised the Committee in 2006 that it would be reducing the fringe benefits tax assessments to nil:

Now that the courts in Essenbourne, Kajewski and Spotlight/Pridecraft P/L have clearly found the arrangements not to be effective for income tax purposes there is minimal risk to the revenue in amending to nil the FBT assessments for cases with similar facts. We expect about 400 cases will be affected with 200 already having been amended to nil.[74]

5.80 The Committee has significant concerns about the ATO’s practice of issuing conditional assessments. The quotation above demonstrates that the ATO issued the assessment based on revenue calculations.

5.81 In the case of employee benefit arrangements, the ATO did have other approaches available. For example, the Full Court in Indooroopilly noted that the ATO would be able to tax the payment of funds from the investment trust (in that case, a Carers’ Share Plan) to the recipients as taxable income.[75] In other words, the ATO was taxing the flow of funds one transaction too early. Given the precedent set in Essenbourne, it would have been defensible for the ATO to argue that it would wait until individual taxpayers received funds from the investment trusts. It could then assess these as income tax and litigate test cases if necessary.

5.82 If the ATO had concerns about issues of fairness in relation to taxing the same transaction twice, it would have had at least two ways of not pursuing the debt. Firstly, in some cases the imposition of fringe benefits tax may have caused hardship on a taxpayer. In Division 340 in Schedule 1 to the Taxation Administration Act 1953, the Commissioner has a general power to release a taxpayer from fringe benefits tax where it would cause serious hardship.

5.83 Secondly, section 34 of the Financial Management and Accountability Act 1997 gives the Minister for Finance and Administration a general power to waive debts due to the Commonwealth.[76] The Committee has previously argued that the ATO should publicly transfer to Treasury responsibility for tax policy questions arising out of litigation. Similarly, transferring a debt collection issue to this Minister is appropriate where there are significant policy and fairness issues about pursuing a tax debt.

5.84 In its submission, Resolution Group made the following recommendation:

The ATO should be prohibited from issuing multiple assessments, either original or amended and whether primary or alternative. The ATO should be required by law to determine the appropriate assessment and only issue and, if necessary, contest that one.[77]

5.85 The Committee would prefer the ATO implemented the spirit of this proposal. Firstly, the Committee wishes to preserve the Commissioner’s discretion where possible. Secondly, when there are many complex transactions, it is difficult to determine which assessment copies another. Rather, the issue with the ATO’s conduct in employee benefit arrangements was that some assessments that were contingent on its success with other assessments. As an implementer of the tax laws, the ATO should determine what the law requires it to assess as income and then pursue these amounts.[78]

Recommendation 14 |

|

|

5.86 |

The ATO amend its policies to limit the practice of issuing assessments that are contingent on each other, and specify in what circumstances such assessments may be validly issued. In the absence of administrative change, the Government introduce legislation to this effect. |

5.87 Over the years, a number of stakeholders have alleged that the ATO is biased towards collecting revenue, rather than collecting tax in accordance with the law. This perception is in the eye of the beholder. The Committee is alert to the fact that such criticisms can be self-serving when made by those caught out as having failed on tax compliance. In its performance audit on rulings in 2001, the ANAO reported allegations by taxpayers that the ATO was biased.[79] The Inspector-General of Taxation has reported that 72% of large corporate taxpayers consider the ATO to be biased in relation to private rulings.[80]

5.88 Sometimes this view is expressed as a perception of bias amongst the community. For example, in RoSA Treasury noted a widespread perception of bias in relation to private rulings. RoSA recommended that the Inspector-General of Taxation investigate this matter.[81] In his recent review, the Inspector-General examined the ATO’s systems and files and found no evidence of bias in the ATO’s private rulings. The Inspector-General confirmed that the perceptions of bias were widespread, but these were due to the way the ATO dealt with applicants. This included requesting taxpayers to withdraw applications, making requests for additional information that did not always appear warranted, and discussing issues with Treasury without advising taxpayers. By not being open with taxpayers about these delay-causing behaviours, taxpayers concluded from the information available to them that the ATO was exercising the sort of bias that would be expected from a revenue agency.[82]

5.89 In its performance audit on rulings, the ANAO was not able to conclude about whether the ATO’s private rulings showed a pro-revenue bias. Rather, the report focussed on whether the ATO’s processes supported robust decision-making:

The ATO rejects this view and it is difficult to determine whether this view is valid…

The ATO disagrees and it is difficult to conclude one way or the other about user/stakeholder perceptions…

We note that some rulings are contentious and we appreciate that views may differ on matters of legal interpretation (sometimes very important matters of legal interpretation) because that is the nature of the interpretative process. However, in view of our discussion and conclusions relating to the public rulings production processes … we conclude that the processes are in place to assure reasonably the legal quality of the ATO’s public rulings.[83]

5.90 The ATO’s third external scrutineer is the Ombudsman. The Committee asked the Ombudsman of the culture of ATO staff and whether they adopted a pro-revenue bias:

If we see the Taxation Office through the prism only of the individual complaints that we receive and the contact we otherwise have, the evidence from that contact does not substantiate the general criticisms that are made. But I think what we do see is that every issue has two sides to it …

There are complaints and difficulties if the Taxation Office has labels that are pejorative such as ‘aggressive tax planning promoter’ or whatever. On the other hand, it says it is failing in its response to calls from the public if it does not do that to differentiate between those who are innocent and genuine, committed and acting in good faith and those who are not. I think that is the general experience that we find. One can point to an issue or an example to substantiate a general point, but it is quickly counterbalanced by experience of a different kind or by imagining what the alternative is going to be if you take the other line.[84]

5.91 The Ombudsman’s point about two sides to every story is very relevant. If a taxpayer disagrees with or engages in a dispute with the ATO and is unsuccessful, they are likely to be dissatisfied. With the support of democratic processes, they are also entitled to complain. Every case where a taxpayer is dissatisfied has the potential to be a public, high profile criticism of the ATO.

5.92 The other side of the story is where a taxpayer disagrees with or engages in a dispute with the ATO and is successful. Any such taxpayer is likely to be satisfied but will have little incentive to announce this outcome. The public is unlikely to hear about these cases. The ATO has publicly stated that it ultimately accepts taxpayers’ arguments in many cases.[85]

5.93 In the view of the Committee, proving systemic bias in the ATO will be methodologically difficult undertaking. The sort of process that would be required would be to take a statistical sample of the ATO’s decisions and then assess whether each one demonstrated a revenue bias, a taxpayer bias, or was neutral. Arguably, for an allegation of revenue bias to be valid, the examples of a revenue bias would need to outweigh the examples of taxpayer bias.

5.94 In An Assessment of Tax, the JCPA argued that, whenever there was doubt over an interpretation of the law, the ATO should give the taxpayer the benefit of the doubt.[86] Under this approach, one decision by the ATO with a revenue bias would arguably be sufficient to demonstrate a revenue bias overall. Clearly, this is not practical. The analysis then becomes an exercise in determining what proportion of the ATO’s decisions is permitted to demonstrate a revenue bias.

5.95 The ATO has already implemented processes to achieve much of this analysis through its technical quality reviews. In these reviews, the ATO selects a statistical sample twice a year of its different types of decisions and then conducts internal peer review. Generally, the ATO’s benchmark for a pass rating is 95%. The ATO achieved a performance of 97.0% for August 2006 to January 2007, up from 95.8% from February 2006 to July 2006.[87]

5.96 If the Committee were to cite the examples of where there may be evidence of a pro-revenue bias, it would raise the following:

n the ATO issuing conditional assessments in employee benefit arrangements

n prior legislative arrangements where the ATO could automatically apply penalties to taxpayers who did not follow private rulings (chapter three)

n the ATO’s conduct in Essenbourne

n the ATO arguing in Walstern that private opinions were not relevant authorities to support a taxpayer’s claim for a reasonably arguable position (chapter three)

n the combination of the ATO’s delays and compliance response in the mass marketed investment schemes.

5.97 The common thread in these examples is fairness. Simply put, the ATO engaged in conduct in these instances that most observers would describe as unfair. However, this does not necessarily demonstrate a pro-revenue bias or a general unfairness on the part of the ATO. This agency makes hundreds of complex decisions daily. To cite five occasions over 10 or more years does not demonstrate bias.

5.98 What these decisions demonstrate is the importance of fairness in dealing with taxpayers and the seemingly disproportionate effect that an unfair decision can have. Each decision has the potential to reduce the reputation of the ATO. This could then affect the number of taxpayers who decide to be compliant and, in turn, could affect the security of the revenue. The ATO itself noted this in its submission where it stated:

Procedural fairness, courtesy and integrity underpin a world class tax administration.[88]

5.99 In the view of the Committee, what would assist the ATO is a mechanism whereby there would be a fairness check on all significant decisions dealing with taxpayers. To some extent, the mechanisms for this are already in place. The ATO has the Taxpayers’ Charter, which requires the ATO to act fairly and reasonably with taxpayers.[89] The ATO also has technical quality reviews. In its 2004 performance audit on the Taxpayers’ Charter, the ANAO recommended that the ATO implement systematic, supplementary quality assurance processes. These processes would include compliance with Charter principles.[90]

5.100 In June 2008, the ANAO finalised a follow-up audit on the Taxpayers’ Charter. The ANAO found that the ATO had met the intent of this recommendation by implementing an integrated quality framework based on recognised standards. The ATO conducted internal consultations to ensure that the framework complies with Charter principles. In time, the framework will replace technical quality reviews.[91]

5.101 While the Committee regards all of the principles in the Taxpayers’ Charter as important, perhaps the most important of them is the ATO’s commitment to act fairly. The Committee trusts that the integrated quality framework will further raise the visibility of this Charter principle in ATO decision-making.

5.102 Compliance work is the most sensitive area of the ATO’s administration of the tax system. The Committee is satisfied that the ATO’s compliance model is a suitable foundation for this because it assists compliant taxpayers and encourages taxpayers in general to comply with the tax laws.

5.103 Much of this chapter has concentrated on how the ATO managed employee benefit arrangements, including the Essenbourne case. Out of all the issues raised with the Committee during the inquiry, the Committee is the most concerned about Essenbourne. It took the ATO four years to accept the Federal Court’s decision in that case. The Committee agrees with Justice McHugh and the Full Federal Court in Indooroopilly that a court decision is the law and should be followed. Either appealing the decision or accepting it and referring the issue to Treasury as a policy matter is consistent with the ATO’s role as an independent administrator of the tax laws.

5.104 The Committee accepts that many of the taxpayers in employee benefit arrangements took a conscious decision to push the boundaries of legal conduct to pay less tax but still enjoy the many public facilities that tax revenue provides. But in Essenbourne, the ATO has allowed its critics to argue that it pushes the boundaries of the law as well. This endangered much of the ATO’s good work in establishing, promoting and being guided by the compliance model.