|

|||

|

|

<< Return to previous page | Parliamentary Joint Committee on Public Accounts and Audit Navigation: Previous Page | Contents | Next Page Chapter 1 Biannual hearing with the Commissioner of TaxationIntroduction1.1 The biannual hearings with the Commissioner of Taxation (the Commissioner) resulted from an inquiry into tax administration undertaken by the Joint Committee of Public Accounts and Audit (the Committee) in the 41st Parliament. This is the eighth hearing that has been conducted. 1.2 The previous hearings have increased scrutiny of the administration of the Australian Taxation Office (ATO) through receiving submissions and then conducting public hearings at which the Commissioner responds to Committee questions. 1.3 Nevertheless, this Committee considers an additional element of scrutiny is warranted. 1.4 Therefore, the Committee has decided to table a report which details the Committee’s findings, areas of concern and suggestions for improvement. The Committee hopes that each subsequent hearing will then provide an opportunity to scrutinise the response of the ATO to the Committee’s previous concerns and recommendations. Conduct of the hearing1.5 The hearing took place in Canberra on Friday, 4 March 2011. A transcript of the public hearing is available on the Committee webpage.[1] Details are also available in Appendix A. 1.6 In addition to evidence taken orally at the public hearing, the Committee also received two written submissions and one supplementary submission. The submissions are listed in Appendix B and are also available through the Committee’s website.[2] 1.7 The Committee wishes to thank those who took part in the hearing through providing written or oral evidence. Committee findings1.8 This report is structured around key themes which the Committee considers are important when discussing administration of the ATO. The Committee intends to pursue these key themes in up-coming hearings and reports and to use them as a mechanism for monitoring the ATO’s performance. The Committee may also modify or add to them in future depending on the emerging issues confronting the administration of Australia’s taxation system. 1.9 The key themes that will be addressed in this report are:

1.10 There will also be a section titled ‘other issues’ which will address issues that are more ‘one-off’ in nature and, while important, may not form part of a continuing process of inquiries and reports. For example, the recent High Court decision regarding tax deductibility of educational expenses for those receiving youth allowance and the applicability of the goods and services tax (GST) to online sales will be addressed in this report. 1.11 Each theme contains several sub-elements which focus on specific issues. Theme 1: Service standards1.12 The ATO’s service standards are publicly stated levels of service that clients can expect from the ATO. The ATO reports on 27 service standards.[3] 1.13 In its submission to the Committee, the ATO stated that it expects to meet its annual benchmarks in all areas except for electronic tax returns for individuals, and two complaints Service Standards.[4] 1.14 The ATO added that as a result of improved staff familiarity with new systems, reduced backlogs of work, improved work processes and a focus on addressing the underlying causes of complaints, the current (2010-11) position is significantly improved over the previous year when the ATO failed 12 Service Standards.[5] 1.15 The ATO also submitted that a review of their Service Standards is underway to respond to government and organisational strategic directions and take into account community expectations.[6] 1.16 The ATO submission contained a useful document which provided a traffic light indication of the ATO’s performance against its priorities from the ATOs Corporate Plan. The Committee questioned the ATO about this traffic light system, and was informed that it was a process whereby the ATO compared its performance against commitments and then reported on it. 1.17 It was not clear how this governance process linked to the reporting on Service Standards, but the Committee notes that traffic lights are not used in the publicly reported information on Service Standards provided on the ATOs website.[7] The ATOs website is difficult to navigate and access information for scrutiny purposes. Further, the ATO stated that it is failing three of its Service Standards; however this did not seem to be reflected in any of the traffic lights in the submission.[8] 1.18 The Committee argues that there is value in utilising this traffic light system consistently across the ATOs publicly reported benchmarks, but in particular when reporting publicly on Service Standards. A traffic light system provides a clear indication of the ATOs performance against each benchmark, in an easy to understand manner, thereby increasing transparency and accountability.

1.19 At the hearing the Committee’s questions focused on the following challenges to the ATO’s ability to achieve their publicly stated Service Standards:

Complaint handling1.20 Members of the Committee acknowledge the relatively high satisfaction rates in response to the ATO’s client satisfaction surveys[9]. In these surveys 83 per cent of people overall, 88 per cent of businesses and 79 per cent of tax agents think that the ATO is ‘doing a good job’.[10] Nevertheless, the Committee noted that in their capacity as representatives of the community Committee Members are often dealing with the remaining 17, 12 and 21 per cent.[11] 1.21 In response, the Commissioner voiced his concern that the ATO relies upon community confidence in it as an organisation to enable it to appropriately perform its role. He added that if the focus is on the relatively small proportion of people and businesses that are unhappy, it may negatively impact on the perception of the ATO within the community and thereby limit its effectiveness as an organisation.[12] 1.22 Notwithstanding the Commissioner’s concerns, the Committee considers that the ATO’s handling of complaints provides a useful insight into the effectiveness of the organisation and therefore the Committee questioned the Commissioner extensively about this issue. Specifically the Committee enquired about:

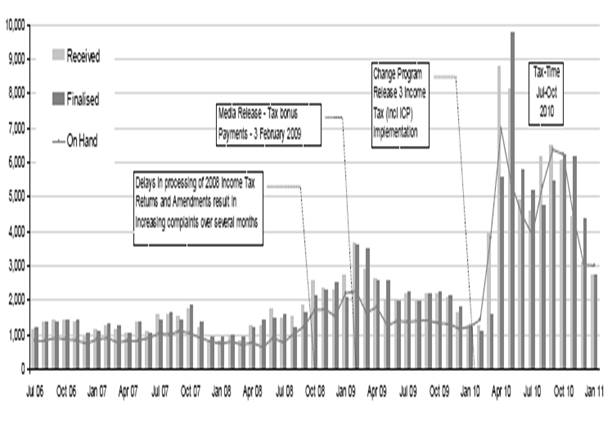

Rise in the number of complaints1.23 The Committee was particularly concerned by the significant increase in the level of complaints that had been received by the ATO directly and also those made to organisations such as the Ombudsman.[13] Figure 1 Complaint Volumes: July 2006 to January 2011

Source Australian Taxation Office, Executive Minute, Response to JCPAA Report 418, p. 6. [14] 1.24 In response, the ATO stated that the large increase in complaints related to two important events namely the tax bonus and the change program. Both of these events resulted in an extraordinary increase in the ATO’s workload. Representatives of the ATO stressed that complaints had been trending downwards in recent times; however they added that there had been a trend towards complaining early on in the process, which may have impacted on the number of complaints being received.[15] 1.25 Members of the Committee sought to understand the number of complaints that were being made by small and micro businesses.[16],[17] The ATO responded that data on specific segments of the market, such as small and micro business, that have made complaints has only become available since the implementation of a new complaints management system as part of the Information and Communication Technology (ICT) change program. Nevertheless, since April 2010 39.4 per cent of complaints were made by micro business and 2.8 per cent were made by Small to Medium Enterprises.[18] 1.26 The Committee was interested to hear what internal tools are utilised by the ATO to monitor complaints and implement changes to the complaints process.[19] The ATO responded that they monitor the number of complaints in order to understand the levels of complaints that are being raised. In addition, the ATO relies upon benchmarking and surveys such as the ‘professionalism survey’ and the ‘community perceptions’ survey to gain an understanding of community perceptions of the organisation.[20] Timeframes for complaints resolution1.27 Members raised concerns about the ability of the ATO to extend the required 21 day timeframe within which complaints must be resolved.[21] The ATO responded that action to resolve a complaint outside of the usual timeframe for complaints resolution must be negotiated with the complainant.[22] 1.28 Committee Members questioned the ATO about the timeframes within which complaints about GST assessments were resolved.[23] The ATO provided information to the Committee which stated that over the past five years the minimum time to resolve a GST dispute was 1 day and the maximum time was 2,094 days. The ATO stated that the maximum timeframe of 2,094 days occurred when the taxpayer concerned requested that a decision not be finalised until the outcome of litigation on similar facts was known. The average resolution time for GST disputes was 161 days.[24] The ATO’s relationship with marginalised Australians1.29 Finally, the Committee was interested to understand how the ATO assisted those people from marginalised communities.[25] Furthermore, Members were interested to know whether there was a staff member within the ATO that was responsible for advocating on behalf of the complainant.[26] 1.30 The ATO stated that all Australians have the same rights to internal escalation if they are unhappy with the treatment they receive from the ATO. Representatives of the ATO added that a recent Ombudsman’s report had found that the ATO’s client complaints area is an example of best practice.[27] The ATO stressed that it attempted to assist those Australians who may be more marginalised. For example, there have been opportunities provided for people to identify themselves as being in financial hardship and requiring a fast refund. 1.31 The Committee heard that an employee at deputy level[28] manages the complaints process and is responsible for analysing trends in complaints and bringing them to the attention of senior management.[29] Committee comment1.32 The Committee appreciates that the majority of clients who deal with the ATO are satisfied with the service that they receive. Nevertheless, the Committee remains concerned about the experiences of those that are not satisfied with the service of the ATO. Moreover, the ATO admits that it has failed to achieve two of its benchmarked service standards related to complaints handling. 1.33 In addition, the Committee is concerned that there has been an increase in the level of complaints both directly to the ATO and to other organisations such as the Commonwealth Ombudsman. The Committee urges the ATO to further improve its complaints handling process, in addition to work to minimise the initial causes of complaints.

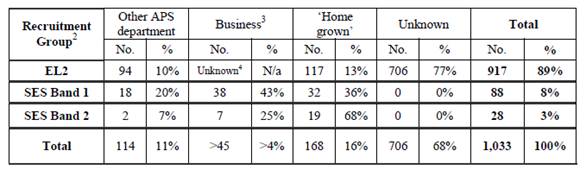

The change program1.34 As has been mentioned above, the implementation of the ATO’s change program had an impact on the number of complaints to the ATO, and its ability to quickly process those complaints. As a result, the Committee spent some time during the hearing questioning the ATO about the change program. 1.35 The change program was a large upgrade to the ATO’s ICT to ensure that it had the capacity to effectively administer taxation and superannuation laws into the future. The program has taken seven years to implement.[30] 1.36 The ATO submitted that the change program has been completed and the new system positions the ATO to provide higher levels of service to the community and also achieves efficiencies for the ATO.[31] At the hearing the ATO added that it had been informed that: ... it is one of the largest system deployments ever put in place in Australia.[32] 1.37 At the hearing the Committee noted that the implementation of the change program had resulted in a spike in the number of complaints made to the ATO in April 2010. The ATO added that as the new integrated core processing system, which was part of the change program, was implemented there were some delays to the processing of refunds which again impacted on the number of complaints it received. To respond to the spike, the ATO had to divert resources from other areas. 1.38 However, the ATO stated that, while the complaint levels over the past 12 months have been higher than normal, the bulk of the complaints that were received during that time period have now been resolved.[33] 1.39 The Committee was interested to hear if the ATO’s ICT systems limit the ability of the ATO officers to efficiently and effectively perform their role. The ATO responded that there was nothing in their current systems which prevented them from performing their role. 1.40 However, the Commissioner did mention that superannuation was a very complex area because of the number of stakeholders that needed to be linked – such as employer, employee, funds and the ATO. He added that the potential changes arising from the Cooper Review in addition to the complexity of the area would require some redevelopment of the ATO’s systems that deal with superannuation. However, while the superannuation ICT system may need improvement, the ATO stressed that it did not currently limit their ability to perform their role.[34] Committee comment1.41 The Committee recognises the large scale of work undertaken as part of the change program. The Committee trusts that the ATO has learned lessons from the implementation of this program which will be used to guide future large scale system changes and improvements. 1.42 The Committee hopes that, as a result of the finalisation of the change program, it will see a substantial decrease in the level of complaints being made to the ATO and the Ombudsman at its next biannual meeting. Tax office culture1.43 A final element upon which the Committee focused at the hearing, in relation to service standards, was the culture of the ATO. Specifically the Committee raised concerns of possible perceived institutional rigidity and a reluctance by the ATO to concede that there may be systemic procedural problems in some of the ATO’s operations.[35] 1.44 At the hearing the Committee repeatedly asked the ATO about areas where the ATO felt that it could improve. While the ATO acknowledged that there was some work to be done, representatives of the ATO tended to stress that, in the main, they believed they were doing a good job.[36] 1.45 The Committee sought information about the recruitment processes for senior staff at the ATO, Executive Level 2 and above, in order to understand whether or not there was ‘groupthink’ at senior management levels.[37] The ATO responded that, for the approximately 22,000 staff in the organisation, it tended to grow people for their career.[38] 1.46 In addition to their response at the hearing, the ATO provided the Committee with more detailed information about recruitment. This additional information stressed that, unlike most Commonwealth departments, over 85 per cent of the ATO workforce is located outside of Canberra. This meant that there was not the same proportionate level of movement of staff across the Australian Public Service as may be the case for other agencies.[39] 1.47 In response to specific queries about the source of staff recruited by the ATO, the Committee was given the following information: Figure 2 Outcomes for EL2 and SES recruitment processes distinguishing between the immediate prior employment source of recruits for the period 2005-111.[40]

Source Supplementary Submission 1.1, Responses to Questions on Notice, Australian Taxation Office, Response to Question No. 9. Committee comment1.48 The Committee was concerned by the ATOs reluctance at the hearing to identify areas where it considered improvement was required and to acknowledge the significance and importance of individual complaints. 1.49 The Committee recognises the Commissioner of Taxation’s concerns that a large factor in the effectiveness of the ATO as an institution is public trust in its ability to perform, and too much focus on the negative may impair its effectiveness. 1.50 However, the Committee does not consider this to be a sufficient reason to limit the identification of areas for improvement. 1.51 The Committee expects, at the next biannual hearing, to see an acknowledgement that ongoing improvements are necessary and that the ATO is making efforts to ensure its culture is one that accepts the importance of complaints and a responsibility for addressing their causes.

Theme 2: Compliance1.52 At the public hearing, the Committee focused on the activities of the ATO aimed at ensuring compliance with Australian taxation requirements. In particular the Committee questioned the ATO about: Ease of compliance1.53 The Committee raised concerns that over 70 per cent of Australians use a tax agent to prepare their tax returns each year, adding that this number was high in comparison to other countries.[45] The Committee questioned the ATO about programs and activities aimed at reducing the reliance on tax agents. 1.54 The ATO responded that there was a significant focus on e-tax and pre-filling of tax returns, assisted by the new ICT which had been implemented as part of the change program, to assist Australians to complete their tax return each year.[46] 1.55 In addition, the ATO stated that it attempted to ensure that communications on its website and administrative arrangements which interpret the tax legislation were practical, in plain English and made sense to people. It was hoped that increased simplicity and ease of use would encourage and facilitate Australians completing their own tax returns.[47] 1.56 The Committee questioned the ATO about the accessibility of its communications, both with businesses and the general public. Members raised concerns that some communications from the ATO were overly complex and difficult to understand. 1.57 The ATO responded that it had and continued to undertake work to improve its communications, and admitted that while it had improved in the area there remained work to be done.[48] Project Wickenby1.58 The Committee enquired as to the success or otherwise of Project Wickenby and what it had cost to administer the program so far.[49] Project Wickenby is a cross-agency taskforce that was established in 2006 to prevent people promoting or participating in the use of secrecy havens.[50] Secrecy havens are also called tax havens and they are countries which have secretive tax or financial systems.[51] 1.59 The Commissioner stated that the first objective of Project Wickenby was to send a signal to those people who use tax havens to try and hide income or assets that they would face consequences for those decisions. He added that another central goal was to provide all Australians with confidence in the administration of the tax system. 1.60 The Commissioner informed the Committee that the amount of money flowing into tax secrecy jurisdictions which had been the focus of Project Wickenby such as Vanuatu, Switzerland and Lichtenstein, has decreased.[52] 1.61 One of the benefits of Project Wickenby, according to the Commissioner, was the success of the coordinated and systematic approach of Australian law enforcement. He added that using cross-agency teams in Project Wickenby had demonstrated benefits that could be used in future, for example addressing issues such as organised crime.[53] 1.62 The ATO submitted that Project Wickenby had cost a total of $295.56 million from its commencement in 2006-07 until 30 September 2010 and of this, the ATO’s direct cost was $164.61 million. The ATO submission added that total collections to 31 January 2011 as a result of Project Wickenby were $574 million.[54] Private equity1.63 In response to questions from the Committee about the rules around private equity, the ATO stated that it was currently consulting with the sector to finalise arrangements aimed at clarifying the requirements and improving transparency in this area.[55] Cash economy1.64 The Committee questioned the Commissioner about his characterisation of the cash economy as a systemic risk. The cash economy refers to the use of cash transactions by people and businesses to deliberately hide income and evade tax obligations.[56] 1.65 The Commissioner responded that by systemic risk he meant that the cash economy is one of those risks that are present in any economy and that there would always be some level of cash payments and non reporting occurring.[57] He added that one of the reasons why the ATO focussed on the cash economy, aside from the fact that it recovered over $200 million in revenue in 2010, was to ensure that businesses that were ‘doing the right thing’ had confidence in the tax system overall.[58] 1.66 The ATO submitted that, while work to address the cash economy formed part of its broad program of work, it also had a specific ‘cash economy program’. The costs of this program were projected to be $34.16 million for the financial year 2010–11.[59] 1.67 The ATO stated that it was seeking to address the risks posed by the cash economy through conducting voluntary disclosure initiatives, where letters were sent to taxpayers encouraging them to disclose their tax liabilities; undertaking more prosecutions and relying on benchmarks across industries to try and monitor and then expose those industries where there may be a hidden economy.[60] Committee comment1.68 The ATO is undertaking a broad range of work to ensure compliance with Australia’s tax system. The Committee commends the ATO for its efforts and successes in this area. 1.69 However, there remains work to be done. A possible focus of the ATO into the future could be on improving the quality of its communication with members of the public, as there are still opportunities to make communications from the ATO more accessible and easier to understand.

Theme 3: Policy development1.70 The Committee questioned the ATO about their involvement in developing policy which had impacts on tax administration. Particular attention was directed at the role of the ATO in simplifying the legislation governing taxation[61] and the level of consultation with the ATO when developing new policies such as tax reform, the carbon tax, the mining tax and the flood levy.[62] 1.71 With regards to questioning about simplification of tax legislation, the ATO stated that legislative changes are the responsibility of Treasury. However, the Commissioner added that where the ATO noticed areas where the law was not operating in accordance with the underlying policy intent, the ATO did bring that to the attention of Treasury. Furthermore, the ATO was attempting to develop administrative arrangements, such as e-tax which, while compliant with the complex legislative arrangements, were user friendly.[63] 1.72 The Committee considers that there is an ongoing discussion currently occurring which is focused on tax administration and tax reform in Australia. In response to questions about the ATO’s involvement in those discussions, the Commissioner informed the Committee that policy discussions were outside of the responsibility of the ATO. However, the Commissioner added that the ATO does seek to provide input on administrative issues such as compliance costs and the administrative feasibility of policy proposals.[64] 1.73 The ATO submitted that they were not consulted on the current proposals for the carbon tax which are being developed by the Department of Climate Change and Energy Efficiency.[65] However, the ATO added that it was ready to respond to the draft cabinet submission, when the draft was circulated for comment.[66] 1.74 According to the ATO, it had quite a high level of involvement in terms of input into the administrative design of the mining tax. The Committee heard that one of the ATO’s deputy commissioner’s has been working with other departments, such as Treasury, on the administrative design of the mining tax, and that work is ongoing.[67] 1.75 Similarly, the ATO stated that it had been consulted in relation to the flood levy and had been involved in its administrative design.[68] Committee comment1.76 The Committee is concerned about the seemingly ad hoc levels of consultation with the ATO when it comes to policy design which will have an impact on the administration of the ATO and the operation of the tax system more broadly. The Committee is not convinced that the current level of consultation with the ATO is sufficiently robust to minimise the impact of those new policies on the administration of the tax system. 1.77 The Committee considers that the ATO has vital expertise and their input should be sought when designing new taxation policies, considering tax reforms or in the simplification of the legislation governing tax in Australia.

Theme 4: External scrutiny and reviews1.78 The Committee discussed the Commonwealth Ombudsman’s report on compromised tax file numbers (TFNs), Australian Taxation Office: Resolving Tax File Number Compromise,[69] with the ATO. The ATO stated that the report focused on nine cases of compromised TFNs out of a potential 3,000 cases and therefore the ATO was concerned that it was not a representative picture.[70] 1.79 The Committee heard that resolving compromised TFNs was fairly complex. The ATO stated that in an environment with heightened sensitivity about identity fraud, it worked hard to make sure that the correct people had the correct identification.[71] 1.80 More broadly, the ATO informed the Committee that in the 2010-11 financial year it was dealing with approximately 24,000 cases of compromised TFNs. Of these, approximately 8,000 to 9,000 had been stolen from an employer. 1.81 In dealing with compromised TFNs, the ATO stated that those which were classed as low risk were managed by putting additional proof-of-identity checks on the system to minimise the need to provide new TFNs. For those that are considered high risk or truly compromised, currently about 900, the ATO issues new TFNs and attempts to reconstruct the account to identify genuine versus fraudulent transactions.[72] 1.82 The Committee queried the level of engagement between the Ombudsman’s office and the ATO. The ATO stated that it sought to meet with the Ombudsman quarterly. 1.83 In addition, when responding to particular reports from the Ombudsman, such as the compromised TFN report, the ATO sought to meet the Ombudsman and brief him on their progress towards implementing his recommendations.[73] Committee comment1.84 The Committee is concerned about the large number of compromised TFNs, and the time taken to resolve this issue. There is a significant potential negative impact on individuals who have been the victim of compromised TFNs. 1.85 The Committee considers that resolution of compromised TFNs should occur as quickly as possible and anticipates hearing of their resolution at the next hearing.

1.86 The Committee intends to become a central monitoring and scrutiny body with regards to the ATO, and as such will pursue greater involvement of external scrutiny organisations. There are a number of agencies who undertake work scrutinising the operations of the ATO including the Australian National Audit Office, the Commonwealth Ombudsman and the Inspector General of Taxation. 1.87 The Committee considers that it has a role to play in monitoring the response of the ATO to reports from these scrutiny organisations. As such, the Committee intends to use the work of these external review bodies at upcoming hearings to help assess the performance of the ATO. 1.88 In addition, the Committee will be seeking public evidence from representatives of these scrutiny bodies as part of the next and following biannual hearings with the Commissioner of Taxation. The Committee will be using the hearings to investigate the links and mechanisms by which these scrutiny bodies work together to scrutinise the operations of the ATO.

Other issues1.89 The Committee questioned the ATO about two additional issues which have been topical and the focus of media attention since the last biannual hearing with the Commissioner of Taxation. These issues were:

1.90 In response to questions about the level of online sales under the $1,000 threshold, the ATO stated that neither it nor the Australian Customs and Border Protection Service had any data which proved or disproved the contention that there has been a significant rise in online sales over the past 12 months.[74] Furthermore, the ATO stated that it had not undertaken any modelling on the amount of revenue that would be raised and the compliance costs of imposing GST on online sales under the $1,000 threshold.[75] 1.91 As a result of the recent High Court decision regarding tax deductibility of education expenses the ATO was writing to all people identified as being eligible and offering automatic amendments to their tax returns of $550 per year going back to 2007-08 financial year. Those identified would not need to provide documentary evidence unless they sought to claim more than the $550 automatic deduction. 1.92 The ATO added that it was working through the proof requirements for upcoming tax returns and that the type of proof needed often depended on the expense being claimed.[76] Concluding comments1.93 The Committee believes additional scrutiny of the administration of ATO has resulted from these biannual hearings. The Committee notes that the Commissioner, in his opening statement: ... welcomed ongoing dialogue with the Committee who we believe can effectively examine the operations of the ATO and provide community insights.[77] 1.94 The Committee in the 43rd Parliament is seeking to enhance its activities with regards to scrutiny of the ATO. As noted above, in order to achieve this goal, the Committee intends to enlarge future biannual hearings to include public evidence from organisations such as the Inspector General of Taxation, the Australian National Audit Office, and the Commonwealth Ombudsman and peak industry or consumer bodies. All of these organisations have expertise upon which the Committee can draw when scrutinising the administration and operation of the ATO. The Committee feels that this will add to the transparency and accountability of the ATO, and further improve its operations. 1.95 Another element of increased scrutiny is that the Committee expects the ATO to provide it with a submission at least a month before the hearing. This will enable Members time to consider the submission and any issues that it raises. 1.96 In addition, the Committee will monitor possible large scale changes to Australia’s tax system, such as the potential impacts arising out of the Tax Forum which is scheduled for later in 2011, to ensure that the ATO is well positioned and also sufficiently supported to implement any changes. 1.97 The Committee wishes to thank those individuals from the ATO who made themselves available to meet with the Committee, particularly the Commissioner of Taxation Mr D’Ascenzo.

Rob Oakeshott MP Chair |

|

||||||||||||||||||||||||||||||||||||